How we built this guide: The pricing examples below are educational estimates based on internal billing observations and external benchmark references. They are not quotes and should not be treated as guaranteed costs.

Actual billed amounts, allowed amounts, and patient responsibility vary by provider, insurer, network status, deductible status, authorization rules, and clinical recommendation. Where possible, we reference external benchmarks from sources such as FAIR Health and federal data. All pricing information is reviewed quarterly and updated as needed.

Major depressive disorder affects roughly 8.3% of U.S. adults in any given year, approximately 21 million people, yet nearly 40% of those with a major depressive episode do not receive treatment (NIMH). Cost is one of the most commonly cited barriers.

Depression treatment cost in New Jersey depends mainly on three things: the level of care you need, whether the provider is in your plan’s network, and how your plan handles deductibles, copays, coinsurance, and prior authorization. For most commercially insured patients, the billed price is not the same as the amount they actually owe.

This guide explains the difference between sticker price, negotiated rates, and out-of-pocket responsibility. It covers self-pay ranges, how coverage typically works, and the questions to ask before committing to a program.

This page is for educational purposes only and should not be treated as medical, legal, or insurance advice. Actual coverage and out-of-pocket costs vary by plan, provider network, authorization requirements, and clinical needs.

What Depression Treatment Typically Costs in New Jersey

If you are trying to estimate depression treatment cost in NJ, start by separating two different numbers: the billed cost of care and the amount you may actually owe after insurance. Those are not the same thing.

The ranges below represent common self-pay or billed-cost reference points across providers in the state. For insured patients, the final amount depends on negotiated rates, deductible status, copays, coinsurance, prior authorization, and whether the provider is in network.

- Outpatient Therapy: Cost of therapy for depression typically ranges from $150 to $300 per self-pay session. Insured patients may owe a copay, coinsurance, or deductible-based share, depending on the plan.

- Intensive Outpatient Program (IOP): For 9–15 hours of care per week, the cost of IOP for depression is roughly $3,000 to $10,000 for a full billed program.

- Partial Hospitalization Program (PHP): For 20–30 hours of care per week, the cost of PHP for depression is roughly $8,000 to $15,000+ for a full billed program.

- Psychiatry: An initial evaluation costs about $200 to $400, with follow-up medication-management visits ranging from $100 to $200.

Here is where the math changes: if you have a commercial insurance plan, you may not necessarily pay those sticker prices. Some plans apply a fixed visit copay, while others apply deductible and coinsurance rules, especially for higher levels of care. Furthermore, if you have Medicaid or Medicare, coverage rules depend on the provider’s participation status and the specific program involved.

For in-network care, patient responsibility is generally based on the insurer’s allowed amount and the member’s cost-sharing terms rather than the full billed charge.

Note: These figures represent approximate billed or self-pay ranges in the New Jersey market. They do not constitute a quote, and they are not a projection of what you will owe after insurance.

How These Ranges Compare to External Benchmarks

Coverage patterns differ by carrier and by plan, but the same variables usually control your real cost: whether the provider is in network, whether you have met your deductible, whether coinsurance applies, whether prior authorization is required, and whether the insurer agrees that the recommended level of care meets medical-necessity criteria.

Three Numbers That Matter (Billed Cost vs. Allowed Amount vs. Your Responsibility)

The biggest mistake people make is assuming the highest number is their only number. To understand the cost of depression treatment, you have to look at three distinct layers of billing.

What the Program Bills (Sticker Price)

This is the billed amount, the total cost for clinical services submitted by the facility to the insurance carrier. While it may look high, this is seldom the amount a patient pays out of pocket.

What Insurance Negotiates (Allowed Amount)

In-network providers like Wellness Hills have contracted rates with insurers. The insurer negotiates the billed amount down to an allowed amount. Your financial responsibility is based on this lower, negotiated number, not the original sticker price.

What You Actually Pay (Out-of-Pocket Responsibility)

Your out-of-pocket responsibility is the final number. This is determined by your specific plan’s deductible, your copayments, and your coinsurance percentages.

What If the Provider Is Out-of-Network?

The three-layer billing explanation above assumes in-network care. If the provider is out of network, your share may be significantly higher, or your plan may not cover the services at all.

Before choosing a provider, confirm these three things with your insurer:

- Does my plan offer any out-of-network behavioral health benefits?

- Is there a separate out-of-network deductible, and if so, how much is it?

- Can the provider supply documentation I can submit for out-of-network reimbursement?

If your plan has limited or no out-of-network benefits, choosing an in-network provider is usually the most cost-effective path.

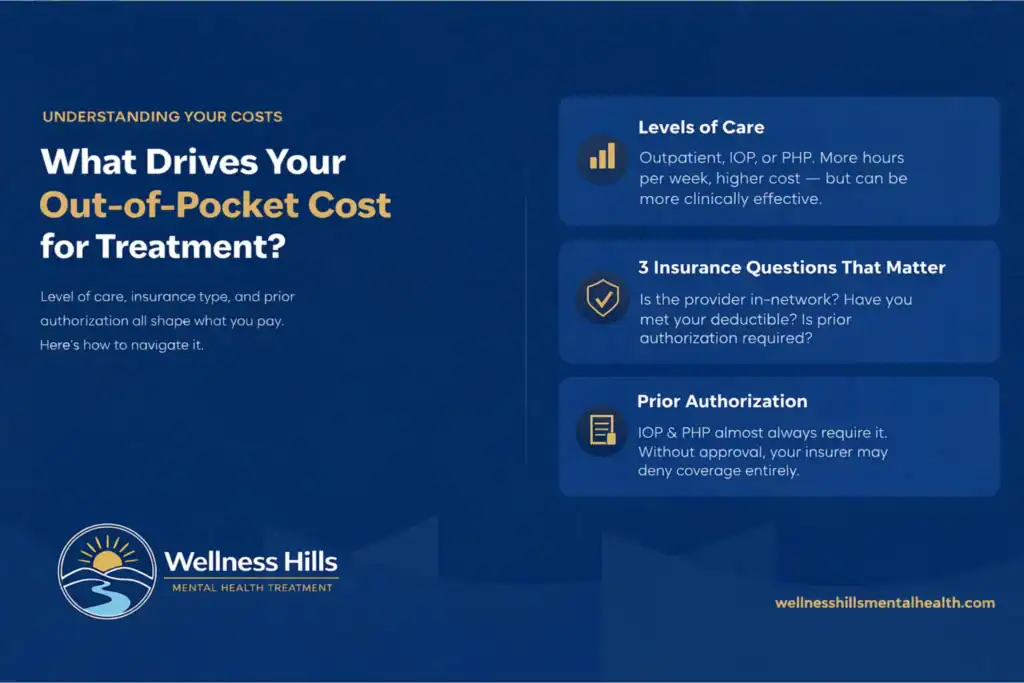

What Drives Your Out-of-Pocket Cost?

Several variables act as dials that turn the price up or down.

Level of Care and Weekly Hours

Generally, the more intensive the program, the higher the billed cost. However, a higher level of care, such as a Partial Hospitalization Program (PHP), might be more cost-effective if it prevents a long-term crisis or hospitalization.

- Outpatient therapy (1–2 sessions per week): Usually the lowest-cost weekly option. It may be appropriate when symptoms are manageable, safety concerns are low, and daily functioning is largely intact.

- Intensive Outpatient Program (IOP) (3–5 sessions per week): A more structured option involving 9–15 hours of treatment for depression per week. It may be appropriate when weekly therapy has not provided enough support, but the person remains safe to live at home and can maintain some daily responsibilities.

- Partial Hospitalization Program (PHP) (full weekdays): A higher-intensity day program involving 20–30 hours per week. It may be appropriate when symptoms are more disruptive, closer monitoring is needed, or the person requires daily clinical structure but does not need overnight hospitalization.

A lower weekly price does not always mean the best overall value. In some cases, a more structured level of care can be more efficient clinically and financially, but treatment duration and response vary by person, and the right level of care should be determined by clinical assessment, not cost alone.

The Three Insurance Questions That Matter Most for Depression Treatment Cost

You don’t need to memorize every plan label to estimate your likely cost. Start with these three questions:

- Is the provider in network for my specific plan? In-network care is almost always less expensive because the insurer has pre-negotiated rates with the provider.

- Have I met my deductible, and does coinsurance apply to IOP or PHP? For structured programs, your cost-sharing may be coinsurance-based (a percentage of the allowed amount) rather than a flat copay.

- Does my plan require prior authorization for structured mental health treatment? Most plans require it for IOP and PHP. Without authorization, the insurer may deny coverage entirely.

Plan type (PPO, HMO, EPO) still affects your options. PPO plans typically allow out-of-network access, while HMO plans usually require referrals and in-network care only. Still, the three questions above usually affect your out-of-pocket estimate more directly than the plan label alone.

If you purchased your plan through the NJ Health Insurance Marketplace (GetCoveredNJ), your coverage level depends on your metal tier. All marketplace plans are required to cover mental health services as an essential health benefit under the ACA, but Bronze plans have the highest per-visit costs, while Gold and Platinum plans have lower per-visit costs with higher premiums.

Prior Authorization

Structured programs like IOP and PHP almost always require prior authorization. This is a clinical review in which the insurer confirms that the treatment is a medical necessity. At Wellness Hills, we submit the clinical documentation required for prior authorization and communicate the insurer’s determination to the patient.

What Insurance Typically Covers for Depression Treatment in New Jersey

Commercial insurance plans often cover outpatient therapy and may also cover structured mental health programs such as IOP and PHP when medical-necessity criteria are met. However, coverage is not automatic. Network status, authorization requirements, plan design, and the insurer’s clinical review process all affect whether care is approved and what the patient owes.

Two layers of legal protection support more comparable coverage. At the federal level, the Mental Health Parity and Addiction Equity Act (MHPAEA) requires that health plans offering mental health benefits cannot impose more restrictive limitations on those benefits than on medical or surgical benefits.

At the state level, New Jersey enacted P.L. 2019, c. 58 (A2031), which strengthened parity enforcement by requiring all NJ carriers, including individual market plans, small employer plans, and state employee health benefit programs, to cover mental health conditions and substance use disorders under the same terms and conditions as any other illness. The NJ Department of Banking and Insurance (DOBI) oversees compliance, and consumers can file parity-related complaints directly with DOBI.

In practical terms, parity laws are designed to prevent mental health benefits from being managed more restrictively than comparable medical or surgical benefits under the same plan. That can include financial requirements and treatment limitations. However, parity laws do not eliminate deductibles, coinsurance, prior authorization, or utilization review. They affect how those rules may be applied, not whether treatment is free.

That said, coverage is not automatic.

It often depends on:

- Your specific plan

- Whether the provider is in-network

- Whether prior authorization is approved

- How your insurer defines medical necessity

This is where the admissions team comes in.

At Wellness Hills, the process typically includes:

- Confirming your benefits

- Checking your deductible and cost-sharing structure

- Identifying authorization requirements

- Providing an out-of-pocket estimate before you start

Questions to Ask Your Insurer Before Starting Depression Treatment

Before you enroll in any program, call your insurance company and ask these questions. Write down the date, the representative’s name, and any reference number for the call. That documentation helps if you need to clarify benefits or appeal a coverage decision later.

- Is [provider name] in network for my specific plan?

- Does my plan cover outpatient therapy, IOP, and PHP for mental health treatment?

- Do I need prior authorization before starting IOP or PHP?

- What is my annual deductible, and how much of it has been met so far this year?

- After my deductible is met, will I owe a copay, coinsurance, or both?

- What is my out-of-pocket maximum for the year, and how does my plan apply it to behavioral health services?

- If the provider is out of network, do I have any out-of-network reimbursement benefits?

- What clinical documentation is required if coverage is reviewed or denied?

These eight questions will give you a much more accurate picture of your actual cost than any published price range. If you’d prefer help navigating this process, our admissions team can conduct a confidential benefits verification on your behalf at no cost and with no obligation to enroll.

What Insurers Usually Look For Before Approving IOP or PHP

Insurers don’t approve higher levels of care based on one factor.

They usually look at:

- Symptom severity

- Functional impairment (how much daily life is affected)

- Safety concerns were relevant

- Limited response to weekly outpatient therapy

- A clinical recommendation from a licensed provider

If approved, coverage is often reviewed weekly through utilization review to confirm that care is still appropriate.

What Happens If Your Insurance Denies Authorization?

Authorization denials happen. They do not necessarily mean you don’t need treatment; they mean the insurer’s reviewer, based on the information provided, did not approve that specific level of care at that time. Understanding the process in advance removes the panic if it happens to you.

Common Reasons for Denial

Insurers may deny prior authorization for IOP or PHP if the clinical documentation does not meet their specific medical-necessity criteria, the symptoms or functional impairment do not meet their threshold for a higher level of care, or the insurer determines that a lower level of care should be tried first.

The Appeals Process in New Jersey

If your prior authorization is denied, you have the right to appeal:

- Peer-to-Peer Review: Your treating clinician may speak directly with the insurer’s clinical reviewer to discuss the medical necessity of the recommended care.

- Internal Appeal: If coverage is not approved, you or your provider may file an internal appeal. In New Jersey, Stage 1 appeals are generally decided within 10 business days, or within 72 hours for urgent or emergency situations, admissions, continued stays, or similar time-sensitive cases. Some plans also include a Stage 2 internal appeal, which is generally completed within 20 business days, or within 72 hours in urgent situations.

- Independent External Review: If eligible internal appeals are unsuccessful, New Jersey allows independent external review through the state process.

What This Looks Like in Practice

At Wellness Hills, our utilization review department manages the authorization and appeal process on the patient’s behalf. If a denial occurs, we typically initiate a peer-to-peer review within 24-48 hours.

Additional clinical documentation, such as updated symptom assessments or evidence of insufficient response to lower-level treatment, may affect the outcome of a review, but approval decisions are made by the insurer under the applicable appeal process.

If a higher level of care is not approved after appeal, we work with the patient to identify the highest appropriate level of care their plan will cover, so treatment is not delayed while further options are explored.

Cost at a Glance by Level of Care

| Level of Care | Typical Weekly Hours | What Insurance Reviews | What Affects Out-of-Pocket | Typical Duration |

|---|---|---|---|---|

| Outpatient | 1–3 Hours | Clinical Diagnosis | Copay / Deductible | Ongoing |

| IOP | 9–15 Hours | Medical Necessity | Coinsurance / Deductible | 8–12 Weeks |

| PHP | 20–30 Hours | Acute Symptoms | Coinsurance / Deductible / Plan Terms | 3–5 Weeks |

Note: Ranges are approximate. Your actual program duration and cost depend on your specific requirements and insurance plan. Verify your benefits for a personalized estimate.

How to Think About Cost and Level of Care Together

Cost should not be the only factor in choosing a level of care. A lower-intensity option may cost less per week. Still, it may not be the right fit if symptoms are worsening, daily functioning is declining, or weekly therapy has not produced meaningful improvement.

When deciding between outpatient therapy, IOP, and PHP, consider these questions:

- Are symptoms interfering with work, school, parenting, or daily responsibilities?

- Have you already tried weekly therapy for 8–12 weeks without sufficient improvement?

- Are there safety concerns or a need for closer clinical monitoring?

- Can you function safely at home between sessions?

- Do you need medication evaluation or more structured support during the week?

These questions do not replace a clinical assessment, but they can help clarify what level of care is worth discussing with a provider.

Structured programs are usually more expensive per week than individual therapy. In some cases, a time-limited structured program may be more practical than continuing a lower-intensity option that is not producing enough improvement, but overall cost and duration vary by plan design, clinical need, and response to treatment.

If you are currently experiencing thoughts of self-harm or suicide, this is not a cost decision; it is a safety decision. Call or text the 988 Suicide & Crisis Lifeline immediately, or go to your nearest emergency room.

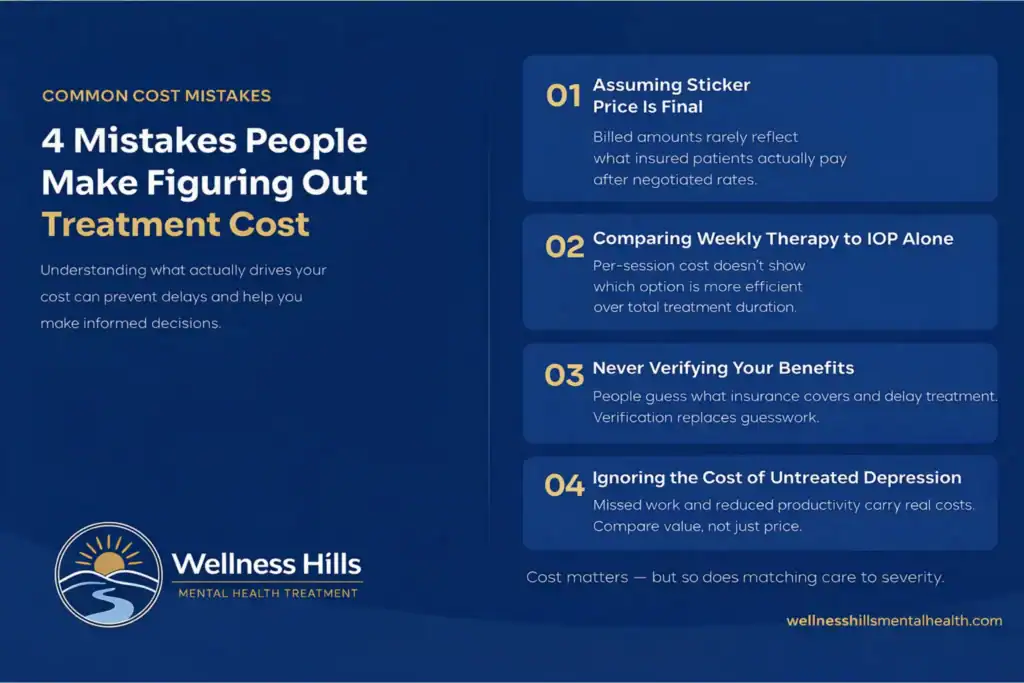

Mistakes People Make When Figuring Out the Cost of Depression Treatment

This is where most people get stuck.

Assuming the Sticker Price Is What You’ll Pay

The billed number is often the highest possible figure. It does not account for negotiated rates or insurance cost-sharing. For insured patients, it’s rarely the final number.

Comparing Weekly Therapy to IOP Without Accounting for Duration and Outcomes

Weekly therapy may cost less per session, but the cost is one of the most commonly cited barriers. The per-session price alone does not tell you which option is more efficient overall. If symptoms continue to disrupt work, relationships, or daily functioning despite consistent weekly sessions, the lower-cost option may not be the most practical fit, and the total cost over time may be comparable to or higher than that of other options.

Never Verifying Benefits Before Making a Decision

People often guess what their insurance will cover, and delay treatment because of it. Verification replaces guesswork with actual numbers.

Not Factoring in the Financial Impact of Untreated Depression

Missed work, reduced productivity, and ongoing care without progress all carry a cost. Cost matters, but so does the functional impact of leaving symptoms undertreated. The right comparison is not only price per week, but also whether the level of care matches the severity of the problem.

What Benefits Verification Looks Like Before Starting IOP: A Walkthrough

To see how the billing process works in practice, consider a hypothetical example based on common scenarios we see at our facility in Chester, NJ.

A New Jersey resident, let’s call him Mark, has an employer-sponsored PPO plan. He has been in weekly therapy for several months, but his symptoms are still interfering with his job and daily functioning. His therapist has recommended a higher level of care, but Mark is concerned about cost.

Step 1: Initial Contact Mark contacts an admissions team (at our facility or any provider he’s considering). During the first call, the team collects his insurance information and begins verification.

Step 2: Benefits Verification The admissions team reviews Mark’s specific plan details and identifies the following:

- Mark’s plan has a $1,500 annual deductible, of which $900 has already been met through previous therapy sessions.

- After his deductible is satisfied, his plan covers IOP at 80/20 coinsurance; the plan pays 80% of the allowed amount, and Mark pays 20%.

- His plan’s annual out-of-pocket maximum is $4,000.

- IOP at this facility is an in-network benefit under his Horizon BCBS PPO plan.

Step 3: Clinical Assessment & Prior Authorization The clinical team reviews Mark’s history and functional impairment. Based on clinical criteria, they recommend IOP. Before Mark starts, the team submits prior authorization documentation to his insurer. This step confirms that the insurer recognizes the medical necessity of the recommended level of care.

Step 4: Cost Estimate Once authorization is approved, Mark receives an estimate of his likely out-of-pocket responsibility. Based on his remaining $600 deductible and his 20% coinsurance on the allowed amount, his estimated total for a 10-week IOP program is approximately $1,200–$1,800. He chooses the evening IOP schedule so he can continue working during the day.

Step 5: Ongoing Review & Step-Down Throughout his program, the facility handles weekly utilization reviews with the insurer. When Mark’s clinical team determines he’s ready, he transitions to outpatient care, which is less intensive and has a lower weekly cost.

This walkthrough reflects a hypothetical scenario based on common patterns. It is not a cost guarantee. Your actual cost depends entirely on your specific plan’s rules, negotiated rates, deductible status, and the outcome of any authorization.

Payment Options If You Are Uninsured or Underinsured

If you don’t have insurance or your plan leaves you with high out-of-pocket costs, you still have options worth exploring.

Self-Pay Options

Ask any provider you’re considering about their self-pay rates, whether installment plans or payment arrangements are available, and whether lower-intensity services might be a financially realistic starting point. At Wellness Hills, our admissions team can walk you through transparent self-pay rates and discuss payment arrangements based on your specific program and situation.

Medicaid, Medicare, and Public Resources

If you have Medicaid or Medicare, confirm whether the provider you’re considering participates with your plan. Wellness Hills does not currently accept Medicaid or Medicare, but New Jersey has several publicly funded pathways to mental health care:

- NJ Mental Health Cares: 1-866-202-HELP (4357) – A state-funded service that connects uninsured and underinsured NJ residents with local mental health providers, including community mental health centers that may offer sliding-scale fees.

- NJ FamilyCare (Medicaid): If you qualify based on income, NJ FamilyCare covers mental health services at little or no cost through participating providers.

- Federally Qualified Health Centers (FQHCs): FQHCs are required by law to provide care regardless of ability to pay, using a sliding fee scale based on income. Find one near you through HRSA’s Find a Health Center tool.

- SAMHSA Treatment Locator: Search for mental health treatment providers in New Jersey, filtered by payment options, at findtreatment.gov.

- NJ Division of Mental Health and Addiction Services (DMHAS): Oversees the state’s public mental health system. For information on state-funded programs, visit nj.gov/humanservices/dmhas.

24/7 Crisis Resources

If you are in immediate danger, call 911. For mental health-related distress, these services are available around the clock:

- 988 Suicide & Crisis Lifeline: Call or text 988.

- NJ Hopeline: 1-855-654-6735 – Peer support and crisis counseling for NJ residents.

- Crisis Text Line: Text HOME to 741741.

What Makes Depression Treatment Cost Different in New Jersey

New Jersey has stronger parity protections than many states. Under P.L. 2019, c. 58, all NJ carriers, including individual market, small employer, and state employee plans, must cover mental health conditions under the same terms as any other illness. The NJ Department of Banking and Insurance (DOBI) enforces compliance and accepts parity-related complaints from consumers.

That said, the parity law does not set prices. The most important cost variables remain plan-specific: network participation, deductible status, authorization requirements, and your insurer’s definition of medical necessity.

For New Jersey residents, the most practical steps before choosing a program are: (1) verify whether the provider participates with your specific plan, (2) confirm whether structured care requires prior authorization, and (3) ask your insurer for your actual cost-sharing terms for behavioral health treatment at that provider.

Frequently Asked Questions About the Cost of Depression Treatment in New Jersey

The questions below address the most common decision points patients and families raise before starting depression treatment at Wellness Hills, including how therapy modalities are selected, when a more structured level of care is appropriate, and what role medication plays in the overall plan.

Does insurance cover depression treatment in New Jersey?

Commercial insurance plans often cover outpatient therapy and may also cover structured programs such as IOP or PHP for depression. However, coverage depends on your plan’s network rules, cost-sharing structure, authorization requirements, and the insurer’s medical-necessity review.

Does insurance cover IOP for depression in New Jersey?

Often, but not automatically. Many commercial plans may cover IOP when the provider is in network, the plan includes that level of behavioral health coverage, and the insurer agrees that medical-necessity criteria are met.

Does Wellness Hills accept Medicaid or Medicare?

Wellness Hills does not currently accept Medicaid or Medicare. However, NJ FamilyCare (Medicaid) covers mental health services through participating providers statewide, and we can help connect you with appropriate resources.

How much does therapy for depression cost without insurance?

The typical self-pay rate for individual therapy in New Jersey ranges from $150 to $300 per session.

Does Wellness Hills offer payment plans for depression treatment?

Ask our admissions team about current self-pay and installment options. Availability and terms depend on the program and your specific financial situation.

Next Step: Get the Numbers Before You Decide

If you’re trying to determine whether treatment is financially realistic, don’t rely on published price ranges alone. Before starting care, confirm your network status, deductible status, authorization requirements, and likely out-of-pocket responsibility using the questions listed earlier in this guide.

If you’d prefer help navigating those details, you can request a confidential benefits verification through our admissions team. The process is free, there is no obligation to enroll, and the goal is to give you clear numbers before you commit to a program.

Sources:

Major Depression | National Institute of Mental Health (NIMH) – Provides national statistics on major depressive episodes in adults, including prevalence and treatment rates in the United States.

Get Covered New Jersey | New Customers – Explains New Jersey’s official health insurance marketplace, including how residents can compare plans, apply for financial help, and review eligibility for Marketplace coverage and NJ FamilyCare.

The Mental Health Parity and Addiction Equity Act (MHPAEA) | CMS – Explains federal mental health parity protections and how mental health and substance use disorder benefits must be treated comparably to medical and surgical benefits under applicable plans.

P.L. 2019, c. 58 (A2031 ACS/2R) | State of New Jersey – New Jersey parity law addressing health insurance coverage for mental health conditions and substance use disorders.

New Jersey Department of Banking and Insurance (DOBI) – Official state agency for insurance oversight, consumer information, complaints, and Get Covered New Jersey administration.

988 Lifeline – National crisis resource offering call, text, and chat support for people in emotional distress, suicidal crisis, or mental health emergencies.

Find a Health Center | HRSA – Federal locator for HRSA-funded health centers, including community health centers that may offer lower-cost or sliding-scale care.

FindTreatment.gov – Federal treatment locator for mental health and substance use disorder services, with searchable treatment options and support resources.

Division of Mental Health and Addiction Services (DMHAS) | New Jersey Department of Human Services – New Jersey state resource for mental health services, crisis assistance, consumer resources, and publicly funded behavioral health programs.

Welcome to NJ FamilyCare – Official New Jersey Medicaid resource explaining eligibility, enrollment, health coverage options, and how qualified residents can access low-cost or no-cost healthcare benefits.

Editorial Standards

Our Editorial Policy

Our editorial standards keep our mental health content accurate, compassionate, and evidence-informed. Articles are developed using credible sources, reviewed for medical accuracy when needed, and regularly updated.